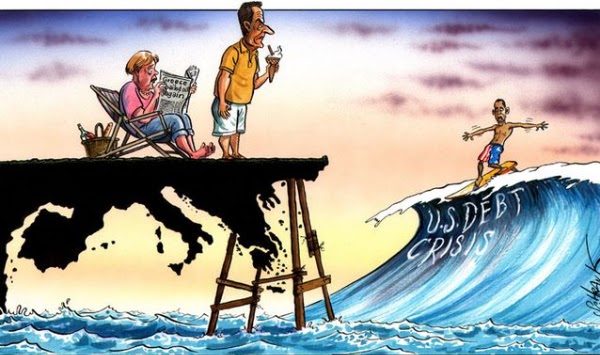

Nowadays the media are painting a bleak picture of the European Union debt crisis. The EFSF has been leveraged, the proposed "hair-cut" on Greek debt has been twisted and turned on all sides, without any visible conclusion. Contagion from the perypheral countries (PIGS) may spread out to the more stable countries: Germany and France (which is already on a credit downgrade outlook from Moody's). Meanwhile the US debt crisis tidal wave is closing by without anyone noticing.

Europe: stop testing the waters and dive right in!

The sheer circus purpetrated by the EU officials, with nine meetings in five days, has been the center of the recent media coverage. There finance ministers have been struggleing to reach an aggreement on the EFSF (European Rescue Fund) that would put Greece out of the sharky waters. According to Reuters, the most recent draft involves "bond insurance" and "special investment vehicles" tailored for every country's needs.

The bond insurance would act like the Credit Default Swaps on sovereign debt (instruments which were recently banned by the EU regulators) and the SPIVs would be used for bond repurchases and bank recapitalisation. More from Reuters:

Under the SPIV scheme, one or more vehicles would be set up either centrally or in a beneficiary member state to invest in sovereign bonds in the primary and secondary markets.Its structure -- the senior debt instrument could be credit rated and targeted at traditional fixed income investors -- is meant to attract international public and private investors, according to the paper.

"The SPIV ... would aim to create additional liquidity and market capacity to extend loans, for bank recapitalization via a member state and for buying bonds in the primary and secondary market with the intention of reducing member states' cost of issuance," the paper said.

The SPIV would be funded by freely traded instruments, such as senior debt and participation capital instruments. The EFSF would also invest in this, and would absorb the first proportion of losses incurred by the vehicle if a state defaulted.

Some sort of an agreement will be reached at one point, but the main issue today is the slow pace with which the finance ministers are working on the EFSF. There are concerns that the final draft of the paper may be "too little, to late" and would just tread the waters. However, a decicive conclusion in this matter would shift the attention from the EU debt crisis to the more imminent one.

The US have already dived in and are surfing the wave

In all the EU mess and chaos, the media coverage of the US debt crisis asymptotically reached the zero level, and most of the CNBC bubble talk financial pundits forgot about the debt ceiling mockery that occured in August. It will come as a surprise that by the 23rd of November this year, the US congress will have to agree on a $1.2 trillion in automatic spending cuts, mostly in discretionary spending, the US credit rating will be downgraded by Moody's or Fitch. A research paper from BOA Meryl Lynch forecasts that in case of an disagreement the shit will hit the fan:

"The United States will likely suffer the loss of its triple-A credit rating from another major rating agency by the end of this year due to concerns over the deficit, Bank of America Merrill Lynch forecasts.

The trigger would be a likely failure by Congress to agree on a credible long-term plan to cut the U.S. deficit, the bank said in a research note published on Friday"

So, who do you think is the weakest link ?

Snippet Photo from The Independent

No comments:

Post a Comment